Overview

This project focuses on the structured understanding of heterogeneous financial data (news, reports, corporate announcements) alongside multi-agent interaction. By blending agentic workflows with quantitative finance, we build reliable intelligent systems for investment research, risk control, market making, and research of specialized mechanisms in Polymarket.

Motivation

Modern finance is defined by complex mechanisms (like prediction markets) and massive streams of text and data. Traditional models struggle to capture human behavioral dynamics or connect real-time qualitative information with quantitative execution. This project explores how Large Language Models (LLMs) and Multi-Agent systems can automate complex financial workflows, optimize market efficiency, and simulate economic behaviors by treating AI agents as autonomous market participants.

Current Technical Direction

Robust Design and Market Making in Prediction Markets

We study mechanism design and automated market-making (AMM) strategies in prediction markets like Polymarket. The team develops algorithms that combine LLM sentiment analysis with reinforcement learning to optimize liquidity provisioning, while explicitly evaluating system robustness against event-driven volatility and market manipulation.

Agent-Based Financial Market Simulation

We build sandbox environments populated by autonomous LLM agents acting as traders, investors, and regulators. This multi-agent framework allows us to simulate macro market phenomena, analyze price discovery under varying information velocities, and stress-test financial systems against black-swan events.

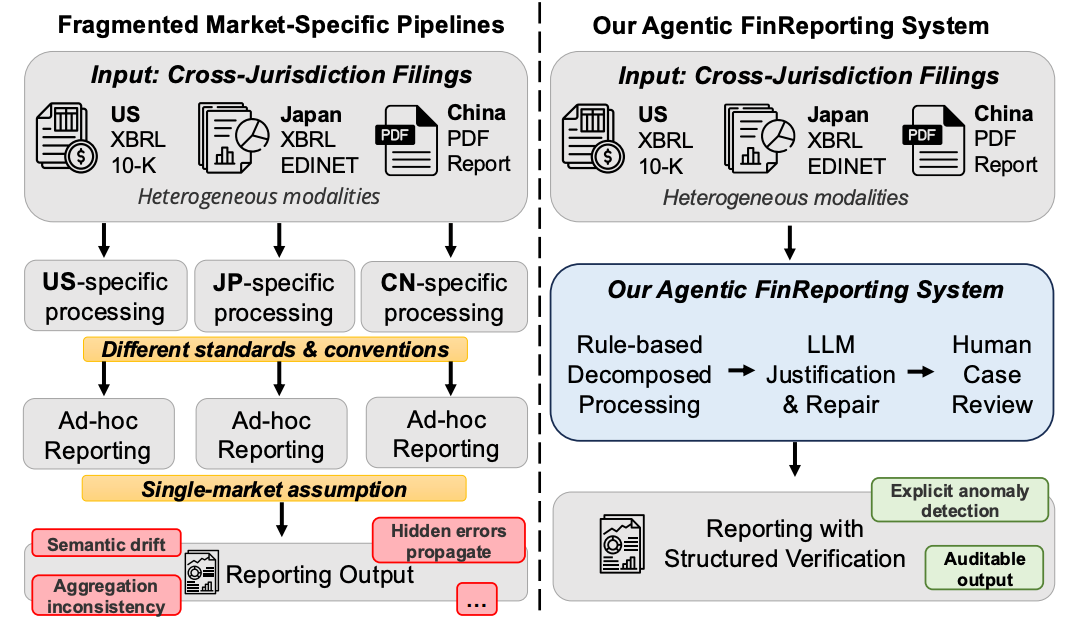

Agentic Financial Reporting and Auditing Services

We construct multi-agent workflows to automate specialized financial services, such as cross-jurisdiction disclosure analysis and compliance auditing. Utilizing frameworks like FinReporting and FinAuditing, the system transforms dense, heterogeneous documents into localized, human-verifiable financial reports.

Related Publications

-

FinReporting: An Agentic Workflow for Localized Reporting of Cross-Jurisdiction Financial Disclosures

Fan Zhang, Mingzi Song, Rania Elbadry, Yankai Chen, Shaobo Wang, Yixi Zhou, Xunwen Zheng, Yueru He, Yuyang Dai, Georgi Georgiev, Ayesha Gull, Muhammad Usman Safder, Fan Wu, Liyuan Meng, Fengxian Ji, Junning Zhao, et al.

ACL Demo Track · 2026

-

FinAuditing: A Financial Taxonomy-Structured Multi-Document Benchmark for Evaluating LLMs

Yan Wang, Keyi Wang, Shanshan Yang, Jaisal Patel, Jeff Zhao, Fengran Mo, Xueqing Peng, Lingfei Qian, Jimin Huang, Guojun Xiong, Yankai Chen, Víctor Gutiérrez-Basulto, Xiao-Yang Liu, Xue Liu, Jian-Yun Nie

SIGIR · 2026

-

Conv-FinRe: A Conversational and Longitudinal Benchmark for Utility-Grounded Financial Recommendation

Yan Wang, Yi Han, Lingfei Qian, Yueru He, Xueqing Peng, Dongji Feng, Zhuohan Xie, Vincent Jim Zhang, Rosie Guo, Fengran Mo, Jimin Huang, Yankai Chen, Xue Liu, Jian-Yun Nie

SIGIR · 2026

Impact Holders

Impact holders and user communities will be added as the project scope becomes clearer.